Law & Commerce is a reporting institution under the Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (Act 613). Law & Commerce also abides by its own Code of Practice, Code of Practice of the Association of Labuan Trust Companies as well as internationally accepted good practice in anti-money laundering and counter-terrorist financing. Law & Commerce places utmost importance on compliance and will only proceed with client’s engagement when due diligent is satisfactory.

Law & Commerce is obligated by the laws to only enter into business relationship when due diligent has been conducted. There are two types of due diligent exercises namely;

Enhanced Due DD must be conducted before entering into business relationship with customers coming from High Risk Countries. If you are national from a listed High Risk Country, you are advised to consult our Compliance Officer to understand our Enhanced Due Diligent requirements.

For Basis Customer Due Diligent (Non-High Risk Countries) before entering into a business relationship with any client we require that at least the following are information;

| 1 | AFGHANISTAN | 36 | JERSEY | 71 | TURKS AND CAICOS ISLAND |

| 2 | ALBANIA | 37 | KUWAIT | 72 | UGANDA (New) |

| 3 | ALGERIA | 38 | LAOS (LAO PEOPLE'S DEMOCRATIC REPUBLIC – Lao PDR) | 73 | UKRAINE (New) |

| 4 | ANDORRA | 39 | LIBERIA | 74 | US VIRGIN ISLANDS |

| 5 | ANGOLA | 40 | LIECHTENSTEIN | 75 | VANUATU |

| 6 | ANGUILLA | 41 | MALTA | 76 | VIETNAM |

| 7 | ANTIGUA & BARBUDA | 42 | MAURITIUS | 77 | ZIMBABWE |

| 8 | ARUBA | 43 | MOLDOVA | 78 | SYRIA |

| 9 | BAHAMAS | 44 | MONTENEGRO | 79 | YEMEN |

| 10 | BAHRAIN | 45 | MONTSERRAT | ||

| 11 | BELARUS | 46 | MYANMAR (BURMA) | ||

| 12 | BELIZE | 47 | NAMIBIA | ||

| 13 | BERMUDA | 48 | NAURU | ||

| 14 | BOSNIA & HERZEGOVINA | 49 | NETHERLANDS ANTILLES | ||

| 15 | CAMBODIA | 50 | NICARAGUA | ||

| 16 | CAYMAN ISLANDS | 51 | NIGERIA | ||

| 17 | CENTRAL AFRICAN REPUBLIC (New) | 52 | NIUE PANAMA | ||

| 18 | DEMOCRATIC REPUBLIC OF CONGO (DR CONGO) | 53 | NORTH KOREA (DEMOCRATIC PEOPLE'S REPUBLIC OF KOREA) | ||

| 19 | COOK ISLANDS | 54 | PANAMA | ||

| 20 | COTE D’IVOIRE (IVORY COAST) | 55 | PAPUA NEW GUINEA (New) | ||

| 21 | CUBA | 56 | SAMOA | ||

| 22 | DOMINICA | 57 | SAN MARINO | ||

| 23 | ECUADOR | 58 | SÃO TOMÉ AND PRÍNCIPE | ||

| 24 | ERITREA | 59 | SERBIA AND MONTENEGRO | ||

| 25 | ETHIOPIA | 60 | SEYCHELLES SAN MARINO | ||

| 26 | GIBRALTAR | 61 | SOMALIA | ||

| 27 | GRENADA | 62 | SOUTH SUDAN (Republic of South Sudan) (New) | ||

| 28 | GUERNSEY | 63 | ST KITTS & NEVIS ST LUCIA | ||

| 29 | REPUBLIC OF GUINEA (CONAKRY) | 64 | ST LUCIA SEYCHELLES | ||

| 30 | GUINEA-BISSAU | 65 | ST VINCENT & THE GRENADINES ST KITTS & NEVIS | ||

| 31 | HAITI | 66 | SUDAN | ||

| 32 | IRAQ | 67 | TAJIKISTAN | ||

| 33 | IRAN | 68 | THE BALKANS | ||

| 34 | ISLE OF MAN | 69 | THE MARSHALL ISLAND | ||

| 35 | ISRAEL | 70 | TUNISIA |

To proceed with ordering our services please complete the Company Formation Questionnaire, Customer Business Profile and Personal Questions & Declaration. These are important preliminary documents which provides us basic information about yourself and your requirement.

Full payment must be received before any service can be delivered. Payment can be made by telegraphic transfer, cheque or cash. Payment by cheque can be made to ‘Law & Commerce Trust Limited’

Payment by TT in US$ or RM can be made to:

Bank: CIMB Bank Berhad

Swift Code: CIBBMYKL

Beneficiary: Law & Commerce Trust Limited

Please read our Pricing Policy before making any payment.

What assets can be held by a Labuan trust?

Why establish a Labuan trust?

There are many reasons why a settlor may wish to create a Labuan trust but some of the principal ones include those listed below.

Tax Mitigation:

Labuan trusts have traditionally been a very important tax planning device and even today a very high proportion of tax saving schemes involve trusts. When a Labuan trust is established , then there will be no taxes applicable to the assets and income of the trust.

Preservation of Family Wealth:

Labuan trust may be used to own specific assets, for example land or interest in family company which it would be appropriate or practical for a settlor to divide between individuals. The use of the trust will allow relevant individuals to benefit from the assets without being directly interested in the assets or having personal ownership and so preserve the assets intact for future generations.

Avoidance of Probate:

Avoidance of probate can be of significant benefit to settlor, both in terms of tax saving and in preservation of confidentiality. As the legal title to the assets concerned passes from the settlor to the trustee of the Labuan trust at the time the settlement is made, there is no change of ownership when the settlor dies, and this neither will nor probate is required at the time of his death.

Emigration:

When a person and or his family moves from one country to another this is often an ideal time and perhaps the only time to set up a trust to take advantage of the tax, exchange control and other laws of the countries concerned in order to preserve family wealth and flexibility to manage it, and allow the members of the family to enjoy the capital and income in the most advantageous ways.

Protection of Assets:

Since the legal ownership of assets within a trust is vested in the trustee of the Labuan trust and not the in the beneficiaries, the settlor and the beneficiaries have no legal control over the assets. As a result, benefits can accrue where the declaration of wealth are required to be provided by individuals in their own countries. In addition the Labuan trust will also protect at least a portion of a person’s wealth from legal attacks by third persons, as for example in the case of suits based on professional negligence or malpractice.

| Private: | Including discretionary, accumulation and maintenance, life interest and fixed interest trusts. |

| Corporate: | Including pension and employee benefit trusts. |

| Charitable: | Solely for the benefit of charitable organizations. |

| Purpose: | Trusts with no beneficiaries that are established for purposes that are certain, reasonable and possible. |

Modern trust deeds can be tailored to meet your specific requirements. Generally they are worded in the widest possible terms to allow a trustee scope to respond to changing circumstances and requirements.

Discretionary Trusts

The most flexible form of Labuan trust and used in wealth protection and tax planning. A discretionary Labuan trust will normally allow the Trustees to appoint additional beneficiaries or to remove existing beneficiaries, and will usually also allow the Trustees to distribute the income and capital of the trust to the beneficiaries in varying amounts and at various times. When a Settlor establishes a discretionary trust he will generally provide the Trustees with a Letter of Wishes, which provides guidance to the Trustees on how he would like them to administer the trust and manage the assets.

Interest in Possession Trusts

These differ from discretionary trusts in that the beneficiaries will be entitled to receive income and capital from the trust as detailed in the trust deed.

Accumulation and Maintenance Trusts

Almost always established for the benefit of children. The trust deed will specify that the trust fund be used for the education and maintenance of the children up to a certain age with surplus income being accumulated by the trust. Once a predetermined age has been reached the beneficiaries will be entitled to receive income and capital from the trust as detailed in the trust deed.

The Advantages of Labuan Trusts

Private relationship, for example, in most jurisdictions trust deeds are not publicly registered.

Labuan Trust Solutions for Individuals

A trust provides many useful solutions to individuals, some of which are:

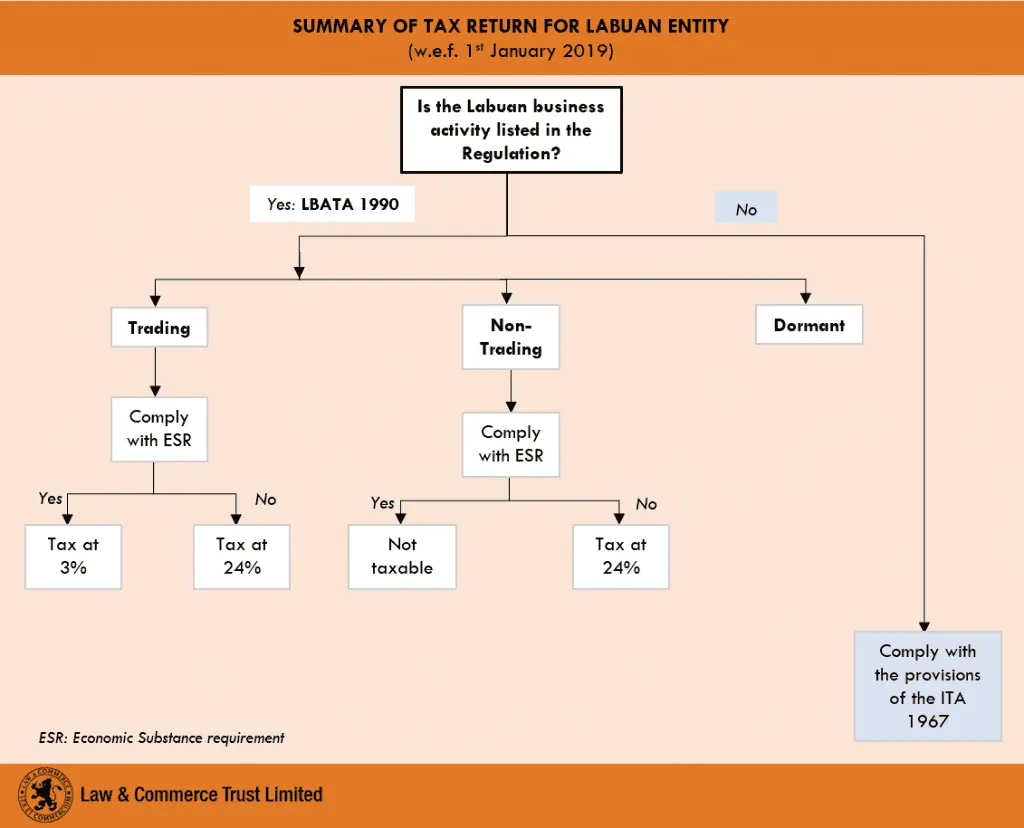

Economic substance regulation (ESR) requires Labuan entities undertaking Labuan business activities to demonstrate that they carry out substantial economic activities in the jurisdictions, in accordance with the Labuan Business Activity Tax Act 1990 (Act 445)

The Labuan entities, as specified in the list shall, for the purpose of Labuan business activity have:

(i) an adequate number of full time employees in Labuan; and

(ii) an adequate amount of annual operating expenditure in Labuan,

as prescribed by the Minister by regulations made under this Act.

The number of full time employees (FTE) and annual operating expenditure (OPEX) varies depending on the type of business activity.

Non-fulfillment of the required ESR, will eliminate a Labuan entity from qualifying for the minimum tax rate of 3% for Trading entities; or 0% for Non-Trading entities.

The full list of Labuan ESR based on business activity can be referred here.

Labuan insurer, reinsurer, takaful and retakaful;

2. Labuan underwriting manager or underwriting takaful manager;

3. Labuan insurance manager or takaful manager;

4. Labuan insurance broker or takaful broker;

5. Labuan captive insurer/takaful;

6. Labuan international commodity trading company;

7. Labuan bank/investment bank/Islamic bank/Islamic investment bank;

8. Labuan trust company;

9. Labuan leasing or Islamic leasing;

10. Labuan credit token or Islamic credit token company;

11. Labuan development finance company or Islamic development company;

12. Labuan building credit or Islamic building credit company;

13. Labuan factoring or Islamic factoring company;

14. Labuan money broker or Islamic money broker;

15. Labuan fund manager;

16. Labuan securities licensee or Islamic securities licensee;

17. Labuan fund administrator;

18. Labuan company management;

19. Labuan international financial exchange;

20. Self-regulatory or Islamic self-regulatory organisations

23. Other trading entity — Labuan entity that carries out administrative, accounting and legal services including backroom processing, payroll services, talent management, agency services, insolvency related services and management services.

21. Labuan entity that undertakes investment holding activities other than pure equity holding activities;

22. Labuan entity that undertakes pure equity holding activities.

From our experience accounting work is rarely expensive and we work with a number of qualified accountants to provide accounting services to your company.

Through our network of qualified accountants, we can offer weekly, bi-weekly, monthly or yearly accounting regular reporting services. Our accounting services covers all aspects of accounting and bookkeeping, including:-

The accountants are familiar with most industry standard software applications, and if required, we can work with other applications also. With our knowledge and experience in Bookkeeping and Accounting procedures we provide our service for all your Bookkeeping and Accounting needs, whether computerized or manual.

We also work with a few well-established audit firms through which speedy and cost-effective auditing may be performed. If you require our recommendation of Labuan approved auditors, please do not hesitate to contact us.

Accounts & audit: A Labuan company must keep its financial records which clearly show its financial position. This would mean keeping accounts up to trial balance at least. As per Labuan FSA, a Labuan company must maintain proper accounting and other records in Labuan. These proper accounting and other records shall be kept at the registered office and shall be open at all times for inspection. A copy of an audited account shall be lodged with the Authority within certain period.

Appointment of auditor: If your company is a trading company, or a non-trading company that does not comply with the required substance, an auditor must be appointed. This auditor must be “a Labuan approved auditor” as listed by Labuan FSA, which could be recommended on your request.

| Taxing statute | Tax rate | Payment deadline | Is account required? | Filing of account to IRB | Filing of account to Labuan FSA | |

| Labuan Trading entities | LBATA 1990 | 3% or 24% | On or before 31st March every year | YES | YES | YES |

| Labuan Non-Trading entities | LBATA 1990 | 0% or 24% | On or before 31st March every year | YES | YES for 24% | NO |

| Labuan entities electing for ITA 1967 | ITA 1967 | Tax rate varies with year of assessment and company’s paid up capital | Advance tax payable monthly | YES | YES | YES/NO |

Major requirements:

In making any new application or renewal of employment pass, Law & Commerce is obligated to make sure that;

To ensure that applicant is genuine and is not purely used as a tool to get residence, Law & Commerce requires the applicant/Labuan company to take the following mandatory services;

A) Law & Commerce’s fee (estimate)

B) Fees payable to Immigration:

A) Employment Pass

Items 1, 8 & 9 will be prepared by Law & Commerce.

B) Dependant Pass

Items 1 & 6 will be prepared by Law & Commerce.

IMPORTANT NOTES: